Broker

After-tax account

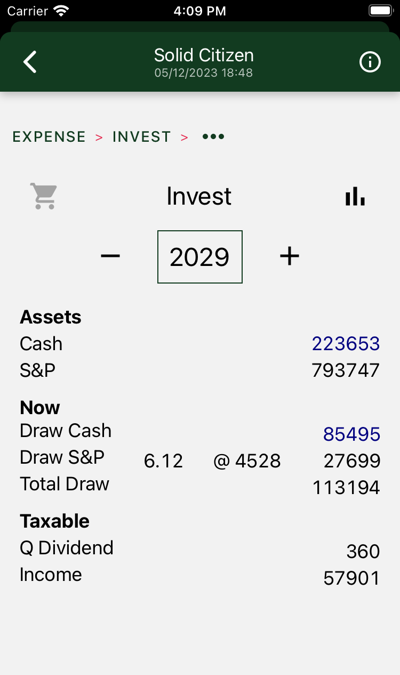

Your assets are divided between after-tax and retirement accounts. Within each account, assets may be held in “cash,” including inflation-protected bonds, or S&P index instruments.

In this year, we draw cash and S&P. Cash draws are denominated in today’s dollars. The S&P withdrawal is denominated in S&P units, or multiples of the S&P average. The dollar figure is an estimate and will vary depending on market performance. Some years you get more, some less.

The draw includes after-tax expenses and estimated tax payment.

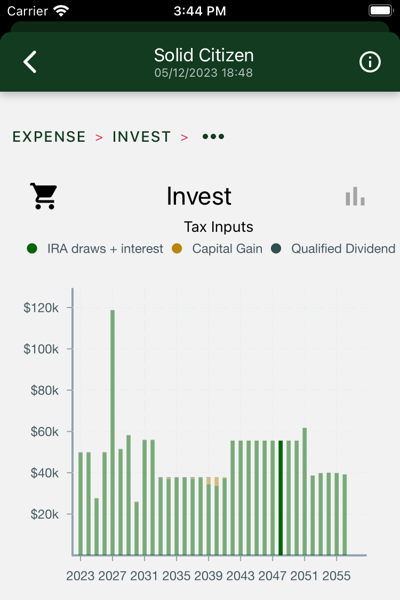

Figures at the bottom show tax imputs from your investments.

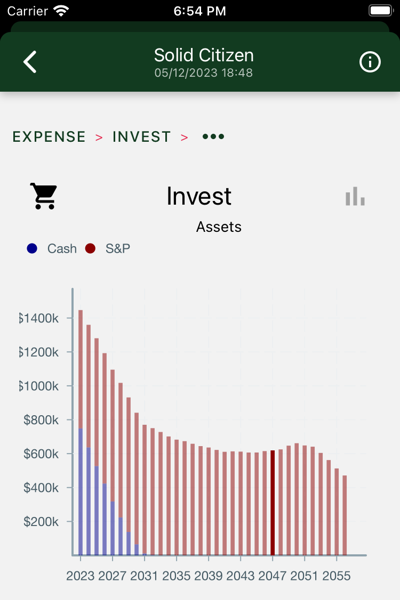

Four charts are shown. Swipe to view each in turn.

Drill down further in results to see similar charts for each separate account. Charts on this page show totals across all of your accounts.

Yearly total account balances, with “cash” and S&P assets highlighted. Cash assets are reserved for the early years, when stock market volatility poses the greatest risk and you don’t have social security to anchor your hedge.

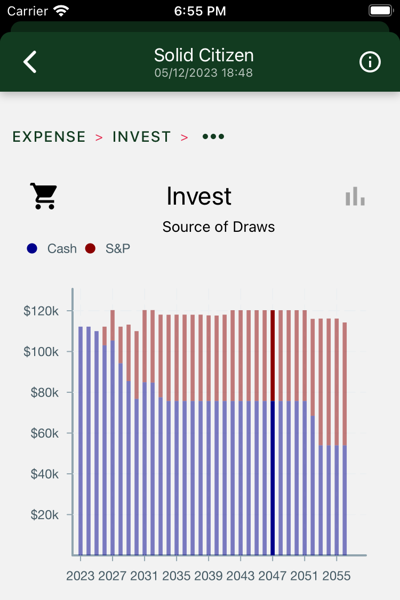

Withdrawals from your investment accounts. Cash assets are consumed first, until the higher expected returns of the stock market catch up to and overtake their expected risk.

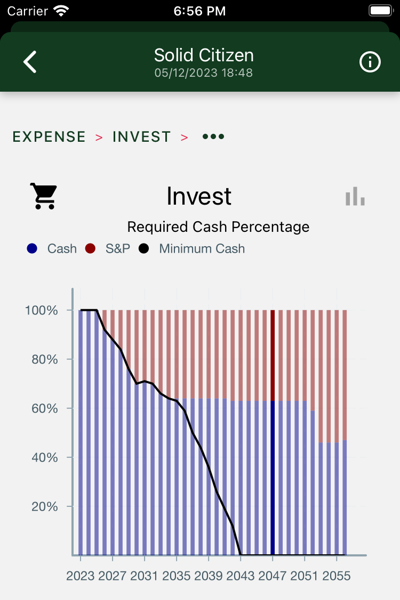

The bars show the percentage of cash assets in each year’s draw. The line shows the required percentage. The bars and line diverge when social security starts, giving you enough cash income to cover your hedge.

These numbers are entered on your tax return. They come from two sources:

In this case, IRA draws are the biggest contributor.