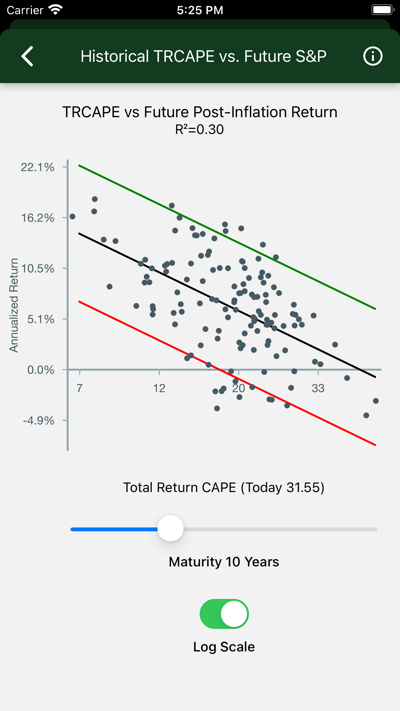

Is past performance any guide to future stock market returns? Efficient market theorists say “no,” but their claims are not universally supported. Robert J. Shiller, the Nobel Prize winning economist, explored this question in 1997, using data you see in this chart.

Data

Each dot on the chart represents a stock purchase made in one year.

-

TRCAPE appears on the x-axis. Computed from ten years of prior Standard and Poors 500 data, it is the ten-yaar average of individual Price/Return ratios, where Price is the inflation adjusted value of the S&P index, and Return is the annualized total real past ten-year return, including reinvested dividends, on the S&P investment. Consider it like a P/E ratio, smoothed over 10 years, and accounting for stock buybacks as well as just earnings. TRCAPE is historically high lately, suggesting that stocks are overvalued. Consult the background material below for how this statistic was developed and named.

-

Annualized Real S&P Return appears on the y-axis. This is the annualized total real return of an S&P investment, including reinvested dividends, over a given Term. It is essentially the sum of the end-of-term price and the compounded reinvested dividends, divided by the original purchase price, transformed into an annualized rate.

-

Term appears in the slider at the bottom of the page. This is the number of years the investment is held. It goes into the computation of data points and the annualized return. As the term increases, returns draw closer to the historical rate of around six percent after inflation.

-

The black line is the best fit. Error bars capture about 95% of the data points. On the logarithmic scale the R-squared statistic is shown. This is interpreted as the percentage of variation accounted for by TRCAPE. An R-squared of zero would appear with a horizontal line, indicating no effect; if R-Squared were 1.0, we would see a perfect fit, with all the dots on the black line.

Interpretation

- With the Term slider in the middle, note that:

- With low values of TRCAPE, returns are high, indicating undervalued stocks.

- With high TRCAPE values, returns drop, indicating overvalued stocks.

- Move the slider to the left. Note that:

- TRCAPE is of little use predicting short-term returns. R-squared (on the logarithmic scale view) is minimal.

- Move the slider to the right. Note that:

- Returns cluster more closely around their predicted values as term increases.

- R-squared initially goes up as the effect of short-term volatility is absorbed and that of TRCAPE is revealed.

- R-squared drops in the out-years, as returns converge on their long-time performance. Even so, the quality of the prediction, measured by the spread of the error bars, continues to increase.

Background

Shiller’s analysis is encapsulated in Valuation Ratios and the Long-Run Stock Market Outlook. Shiller and his co-author, John Campbell, presented his findings to the Federal Reserve Board of Governers December 3, 1996.

In Shillers presentation, he described a statistic he called the “cyclically adjusted price-to-earnings ratio”, abbreviated “CAPE”, “CAPE10”, or “Shiller P/E”. This statistic is computed as the average P/R is described here, except that earnings appear in the denominator instead of total return. This statistic is available daily on financial sites.

As corporations incorporated stock buybacks into their strategies, investors sought a measure that incorporated total return. Shiller responded in 2018 by publishing a “total return CAPE”, or TRCAPE, the measure Hedgematic uses.

Shillers’ publicly accessible papers are linked at Home Page of Robert J. Shiller.

The data displayed on this page is sourced from U.S. Stock Markets 1871-Present and CAPE Ratio.